Imagine this: you’re about to make a payment, and within seconds, your bank quietly checks whether it’s really you. No calls, no delays—just a smooth, secure transaction. But if something seems off, you instantly get an alert, and the transaction is stopped before any damage is done.

This isn’t luck or coincidence—it’s Artificial Intelligence working behind the scenes. Today, AI is transforming banking by making operations faster, decisions smarter, and fraud detection more proactive than ever before. From chatbots that respond instantly to systems that monitor millions of transactions in real time, AI is becoming the invisible force powering modern banking. In fact, according to McKinsey & Company, AI has the potential to generate up to $1 trillion annually in value for the global banking industry, highlighting its growing importance.

AI in Banking Operations

Artificial Intelligence is significantly improving how banks operate by reducing manual effort and enhancing decision-making. One of the most visible changes is in customer service. AI-powered chatbots and virtual assistants are now capable of handling routine queries instantly, offering 24/7 support without long waiting times. This not only improves customer satisfaction but also reduces the workload on call centers and branch staff.

For instance, ICICI Bank uses its AI-powered chatbot iPal to assist customers with instant responses and seamless service, while HDFC Bank has implemented EVA (Electronic Virtual Assistant), which handles millions of queries efficiently. These real-world applications reflect a broader trend—reports by Deloitte suggest that over 70% of banks globally are already adopting AI solutions to improve customer experience and operational efficiency.

AI also plays a crucial role in risk assessment. By analyzing customer behavior, transaction history, and financial data, it helps banks evaluate creditworthiness more accurately. Instead of relying solely on traditional methods, banks can now use predictive analytics to anticipate future behavior and identify potential risks early, leading to smarter and more reliable lending decisions.

Another major impact of AI is seen in workflow automation. Banking processes often involve repetitive back-office tasks such as document verification, transaction processing, and compliance checks. AI streamlines these activities, increasing operational efficiency and allowing employees to focus on more strategic and value-driven work.

In addition, AI strengthens compliance processes, especially in areas like Know Your Customer (KYC) and Anti-Money Laundering (AML). It can quickly scan large volumes of data, detect inconsistencies, and flag suspicious transactions, making regulatory compliance faster, more accurate, and less resource-intensive.

AI in Fraud Detection

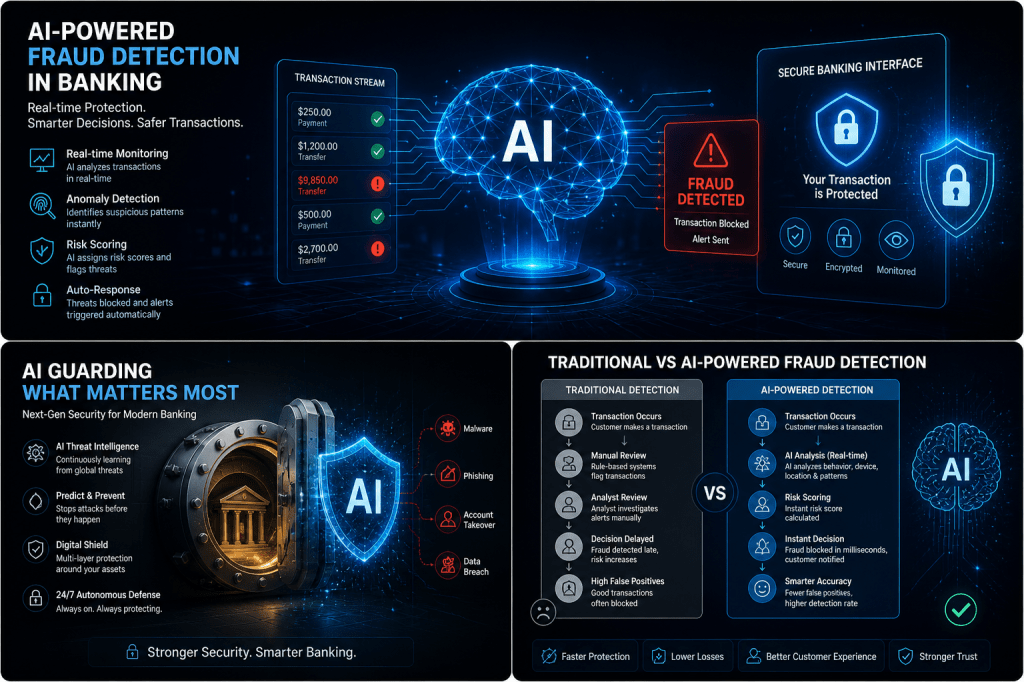

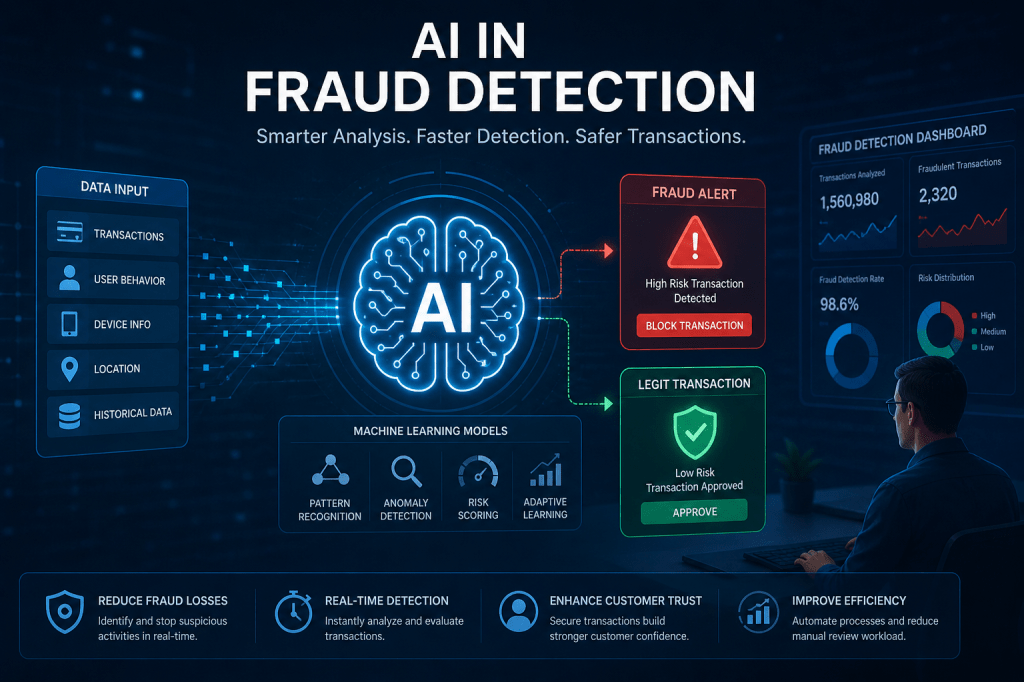

Fraud detection is one of the most powerful applications of AI in banking, where its ability to process large volumes of data in real time makes a critical difference. AI systems continuously monitor transactions and user behavior, allowing banks to detect suspicious activities instantly and take action before financial losses occur. This capability has become especially important in countries like India, where digital transactions are rapidly increasing. According to the Reserve Bank of India, the growth in digital payments has been accompanied by a rise in fraud cases, making real-time AI-driven monitoring essential.

Banks such as ICICI Bank and HDFC Bank leverage AI-driven systems to analyze transaction patterns and detect anomalies instantly, ensuring faster response to potential threats. At the same time, State Bank of India (SBI) uses AI-powered analytics to strengthen fraud detection and anti-money laundering efforts across its vast customer base.

Unlike traditional systems that rely on fixed rules, AI uses advanced pattern recognition to learn from both past fraud cases and normal transactions. This includes supervised learning for identifying known fraud patterns and unsupervised learning for detecting new and emerging threats. As a result, fraud detection systems become more adaptive and effective over time. Studies indicate that AI-driven systems can improve fraud detection accuracy by up to 90%, significantly reducing financial losses.

AI also incorporates behavioral analysis, going beyond transaction details to understand how a user typically interacts with their account. It evaluates factors such as login behavior, device usage, location, and transaction timing. If any unusual deviation is detected, the system can trigger alerts or request additional authentication, ensuring stronger security without disrupting genuine users.

Another important advantage of AI is its ability to reduce false positives. Traditional fraud detection systems often block legitimate transactions due to rigid rules, causing inconvenience to customers. AI, however, learns individual user behavior, making it more precise in distinguishing between genuine and suspicious activities. This leads to fewer unnecessary alerts and a smoother customer experience.

AI is now capable of detecting a wide range of fraud types, including payment fraud, phishing, identity theft, account takeover, synthetic identity fraud, and money laundering patterns. It is also increasingly important in addressing advanced threats such as deepfakes and AI-driven scams, which are becoming more sophisticated and harder to detect.

Benefits for Banks

The adoption of AI provides several advantages for banks. It improves the speed and accuracy of fraud detection, reduces the workload on investigation teams, and enhances overall operational efficiency. At the same time, it contributes to a better customer experience by minimizing transaction delays and false alerts. AI also strengthens compliance systems, helping banks meet regulatory requirements more effectively while maintaining high levels of security.

Challenges to Consider

Despite its many benefits, AI implementation comes with certain challenges. Managing sensitive financial data raises concerns around privacy and security, while biased algorithms can lead to unfair or inaccurate decisions. Integrating AI with legacy banking systems can also be complex and resource-intensive. Additionally, the lack of transparency in AI decision-making makes it difficult to fully explain certain outcomes. For these reasons, human oversight remains essential to ensure responsible and ethical use of AI in banking.

Future of AI in Banking

Looking ahead, the role of AI in banking will continue to expand. Future systems are expected to move towards continuous, real-time risk assessment rather than periodic checks. AI-driven fraud prevention will become more proactive, identifying and stopping threats before they fully develop. At the same time, banks will use AI to offer highly personalized services tailored to individual customer needs. The integration of AI with advanced cybersecurity frameworks will further strengthen the overall resilience of financial systems.

Banks that adopt AI early and responsibly will gain a strong competitive advantage, not only in operational efficiency but also in building customer trust and long-term sustainability.

Conclusion

The next time your bank sends you a quick alert or a transaction goes through seamlessly without a second thought, there’s a good chance AI is working quietly in the background. You may never see it, but it’s constantly learning, adapting, and protecting—making every interaction smoother and safer.

As banking continues to evolve, AI won’t just be a support system; it will become the silent guardian of financial trust. And in a world where fraud is getting smarter, having technology that stays one step ahead isn’t just an advantage—it’s a necessity.