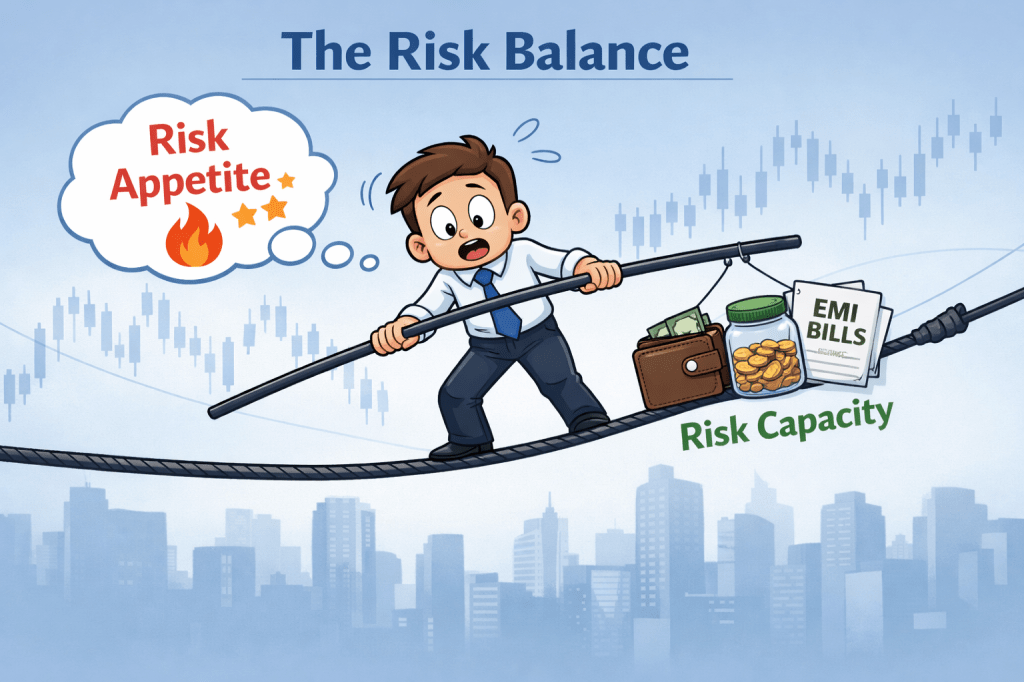

Just because you are willing to take risk doesn’t mean you can afford it.

A young professional invests aggressively in stocks. They believe markets always go up. An entrepreneur quits a stable job. They think risk is necessary for success. A salaried employee takes multiple EMIs, assuming income will keep rising.

Different people. Same mistake.

They confuse risk appetite with risk capacity—and that confusion often leads to financial stress, regret, or long-term damage. Let’s break this down in simple terms.

What Is Risk Appetite?

Risk appetite is psychological. It reflects how comfortable you feel with uncertainty, volatility, and potential loss. Important point: Risk appetite is emotional. In simple words: How much risk are you willing to take?

Examples:

- You enjoy investing in volatile stocks.

- You don’t panic when markets fall.

- You are okay with short-term losses for long-term gains.

Risk appetite is shaped by:

- Personality

- Past experiences

- Confidence (sometimes overconfidence)

- Social influence and peer pressure

What Is Risk Capacity?

Risk capacity is financial. It reflects how much loss you can actually absorb without damaging your lifestyle or goals. In simple words: How much risk can you afford? Important point: Risk capacity is factual.

Examples:

- Do you have an emergency fund?

- Do you have dependents?

- How stable is your income?

- What portion of your money is locked in EMIs?

Risk capacity depends on:

- Income stability

- Savings and assets

- Liabilities and EMIs

- Age and financial responsibilities

Risk Appetite vs Risk Capacity

| Basis | Risk Appetite | Risk Capacity |

| Nature | Psychological | Financial |

| Focus | Willingness to take risk | Ability to bear loss |

| Driven by | Emotions, confidence, mindset | Income, savings, liabilities |

| Changes with mood? | Yes | No |

| Example | “I’m okay with market ups and downs” | “I can survive a 30% loss” |

| Risk of mismatch | Overconfidence | Financial stress |

| Ideal role | Sets direction | Sets limits |

The Most Common (and Dangerous) Mistake:

Many people have high risk appetite but low risk capacity. Typical examples in India:

- Young earners with high salaries but zero savings

- Heavy EMIs (home loan + car + credit cards)

- Aggressive investing influenced by social media

- No emergency fund

They want to take risk—but cannot afford failure. This mismatch is the real reason behind Panic selling in markets, Stress during economic slowdowns, Debt traps and Career burnout, The result?

People take financial risks designed for someone else’s balance sheet.

How to Align Risk Appetite with Risk Capacity

Before taking any major financial decision, ask yourself:

- If this fails, what breaks?

- Lifestyle?

- Savings?

- Peace of mind?

- Do I have a safety net?

- Emergency fund (6 months minimum)

- Insurance coverage

- Am I borrowing to take risk?

- Debt + risk is a dangerous combination

- Is this decision reversible?

- The more irreversible it is, the more capacity you need

Rule of thumb: Your risk appetite can be ambitious, but your risk capacity must be conservative.

Final Takeaway

Risk is not bad.

Avoiding risk completely is also not smart.

But taking risk without understanding your capacity is reckless.

True financial maturity is not about how much risk you take—

It’s about how well your risks fit your reality.